Funding Rates

“Funding is not just a fee. It is a live signal showing which side of the market is crowded.”

Understand crypto perpetual funding, who pays who, and how advanced traders use it for sentiment, risk management, and delta-neutral yield.

FoundationWhat Are Funding Rates?

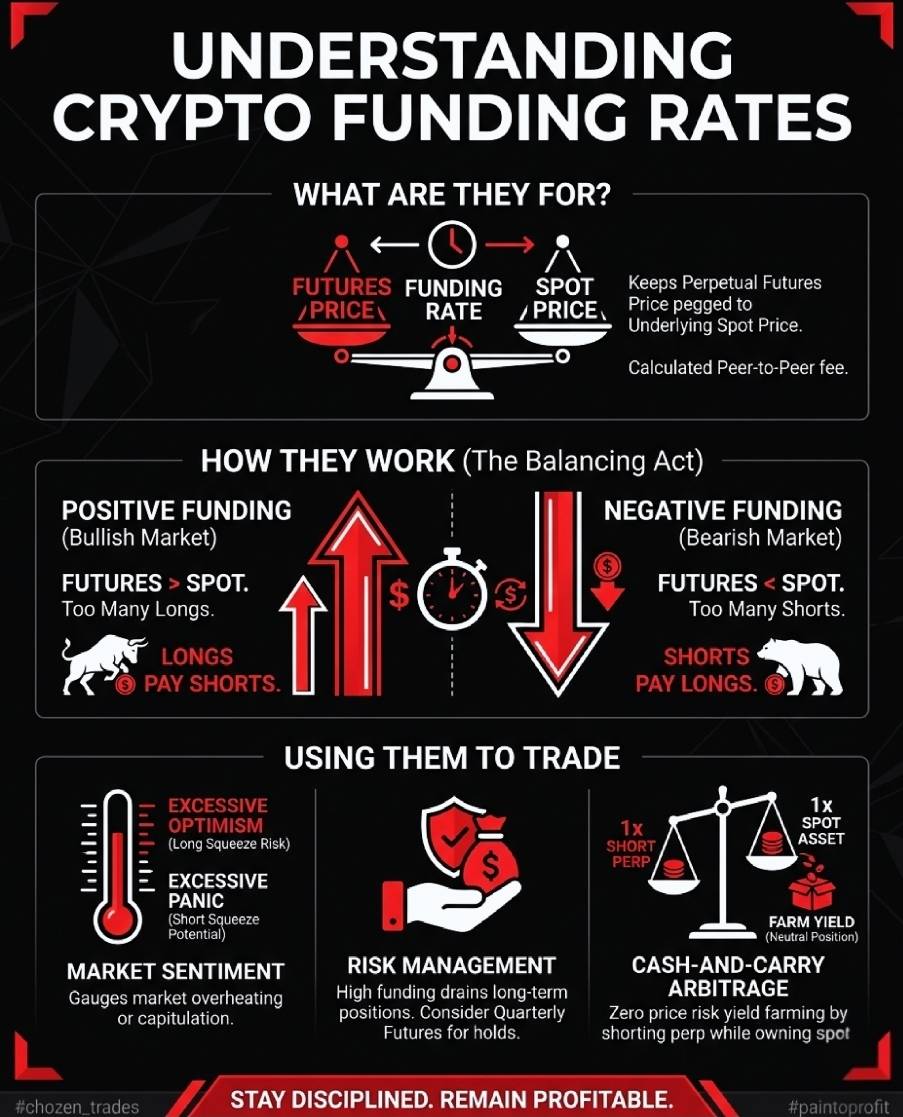

Funding rates are peer-to-peer payments that help keep perpetual futures prices aligned with spot prices.

Foundation

What Are Funding Rates?

Funding rates are peer-to-peer payments that help keep perpetual futures prices aligned with spot prices.

Traditional futures contracts have expiration dates. When expiration arrives, the futures contract settles and the futures price is forced back toward the actual asset price.

Perpetual futures do not expire. Because there is no natural settlement date, exchanges use funding rates to keep the perpetual futures market anchored to the underlying spot market.

Funding is a peer-to-peer fee. The exchange does not keep the payment. It transfers value between long traders and short traders depending on which side of the market is more aggressive.

Perpetual futures can stay open without an expiration date.

Funding helps keep perp prices tied to the underlying spot price.

Funding is paid between traders, not kept by the exchange.

You only pay or receive funding if your position is open when the funding interval settles.

MechanicsPositive vs Negative Funding

The direction of the funding rate shows which side of the market is paying for pressure.

Mechanics

Positive vs Negative Funding

The direction of the funding rate shows which side of the market is paying for pressure.

Positive funding usually means the futures price is trading above spot. This often happens when too many traders are aggressively long. In that environment, longs pay shorts.

Negative funding usually means the futures price is trading below spot. This often happens when too many traders are aggressively short. In that environment, shorts pay longs.

The goal is balance. Funding penalizes the crowded side and rewards the opposite side, helping push the perpetual futures price back toward the spot price.

Positive funding: futures price is above spot, longs pay shorts.

Negative funding: futures price is below spot, shorts pay longs.

High positive funding can signal overheated long positioning.

Deep negative funding can signal panic short positioning.

SentimentUsing Funding as a Market Thermometer

Extreme funding can reveal when leverage is crowded and the market is vulnerable to squeezes.

Sentiment

Using Funding as a Market Thermometer

Extreme funding can reveal when leverage is crowded and the market is vulnerable to squeezes.

Funding rates can be used as a sentiment gauge. When funding becomes extremely positive across the market, it can show excessive optimism and crowded long exposure.

Crowded long exposure can create long-squeeze risk. If price drops, leveraged longs may be forced to close, adding more sell pressure and accelerating the move lower.

The opposite can happen when funding becomes deeply negative. If too many traders are aggressively short, a sharp move higher can force shorts to buy back, creating short-squeeze conditions.

Extreme positive funding can warn of overheated long positioning.

Extreme negative funding can warn of panic short positioning.

Funding does not predict by itself, but it adds context.

The stronger the crowding, the more important risk management becomes.

Risk ManagementFunding Drag and Position Sizing

Funding is calculated on total position size, not just the margin posted.

Risk Management

Funding Drag and Position Sizing

Funding is calculated on total position size, not just the margin posted.

One of the biggest beginner mistakes is thinking funding only applies to margin. It does not. Funding is calculated on the full notional position size.

If a trader uses $100 of margin at 10x leverage, the position size is $1,000. Funding applies to the $1,000 position, not the $100 margin.

High funding can slowly drain a position over time. This matters most for swing trades held across multiple funding intervals, especially during overheated bull-market conditions.

Funding applies to notional position size.

Leverage increases the funding impact because it increases position size.

Small funding numbers can become meaningful over days or weeks.

Longer-term crypto trades may be better suited for quarterly futures when funding drag is high.

Advanced StrategyCash-and-Carry Arbitrage

A delta-neutral funding strategy uses spot and perps together to reduce directional price exposure.

Advanced Strategy

Cash-and-Carry Arbitrage

A delta-neutral funding strategy uses spot and perps together to reduce directional price exposure.

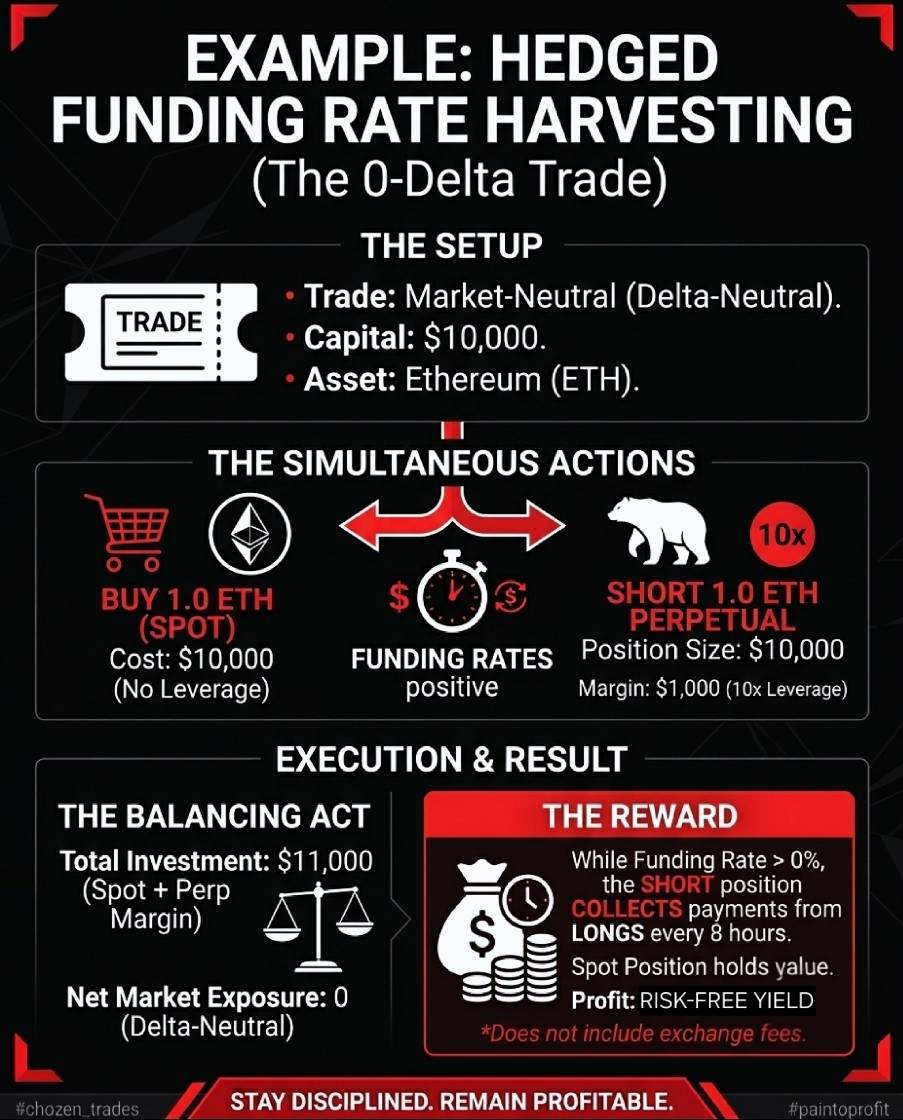

Cash-and-carry arbitrage is an advanced strategy where a trader owns the spot asset and shorts an equal amount of perpetual futures.

For example, a trader could buy $10,000 of spot Bitcoin or Ethereum and open a $10,000 short position on the matching perpetual contract. If the asset rises, the spot position gains while the short perp loses. If the asset falls, the spot position loses while the short perp gains.

The result is close to delta-neutral price exposure. If funding remains positive, the short perpetual position collects payments from long traders while the spot position maintains asset exposure.

This strategy is not risk-free in the real world. Fees, slippage, liquidation settings, exchange risk, borrow conditions, funding changes, and execution errors can all affect results.

Buy the spot asset.

Short an equal notional amount of the perpetual contract.

Positive funding allows the short perp to collect from longs.

Net market exposure is reduced, but operational and exchange risks still matter.

Respect the funding clock. Manage the exposure. Trade the structure.

This material is for educational purposes only and is not financial advice. Perpetual futures, leverage, crypto assets, and funding-rate strategies involve risk, including liquidation risk, exchange risk, execution risk, and loss of capital.