Topic Library

Volatility Shield

“The Volatility Shield is a structured options trading strategy developed by myself that I use almost every single week.”

Founder - Sean Bailey

01OverviewWhat Is the Volatility Shield

Expand

01

Overview

What Is the Volatility Shield

Expand

It combines long-term protective hedging with short-term opportunistic trades to navigate volatile, tech-heavy markets effectively.

At its core:

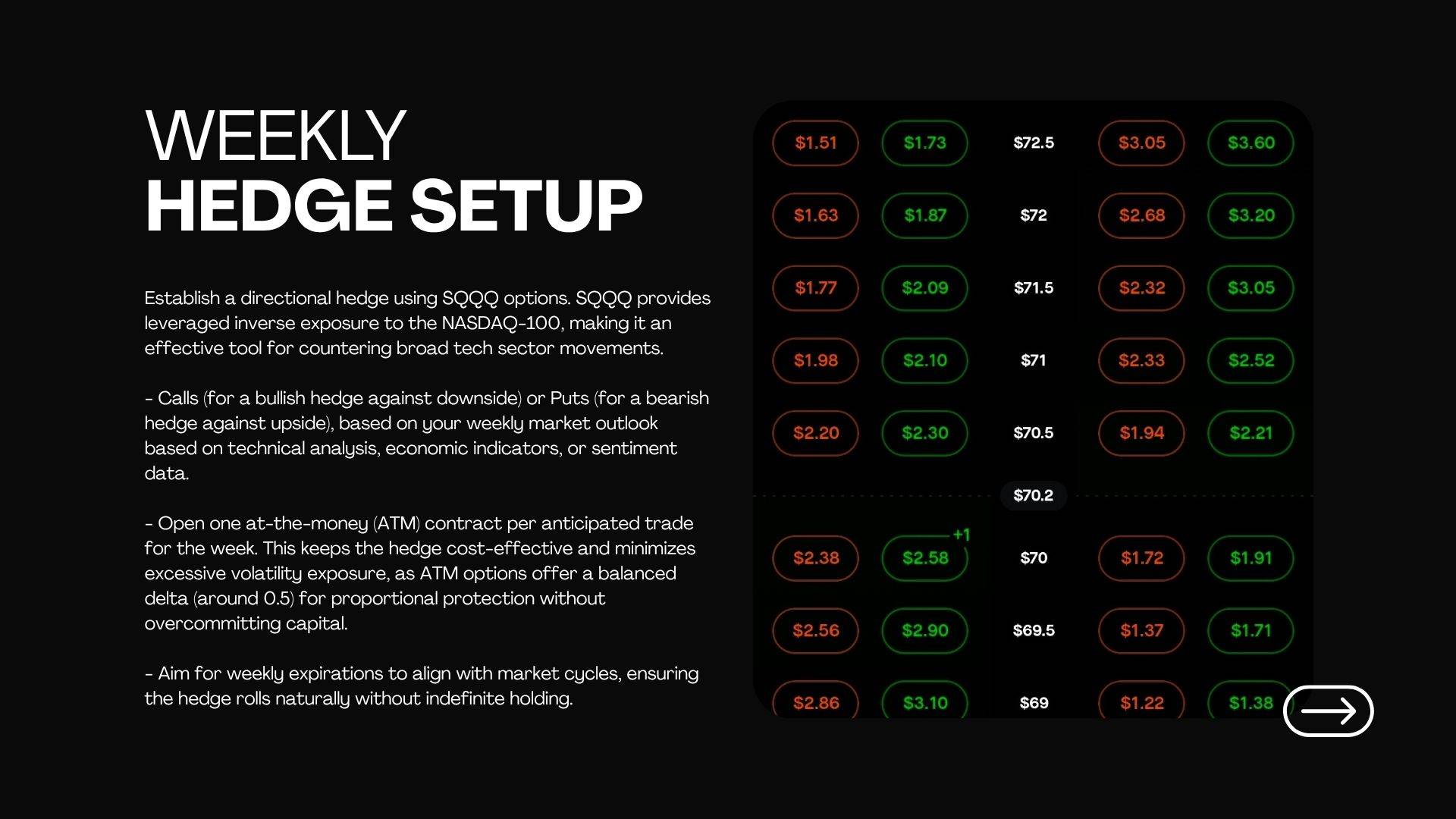

Each week, you establish a directional hedge using one at-the-money (ATM) SQQQ options contract (calls for bearish protection or puts for bullish hedging), based on your weekly outlook for the Nasdaq/tech sector. This acts as a stable, low-volatility shield against broad market swings.

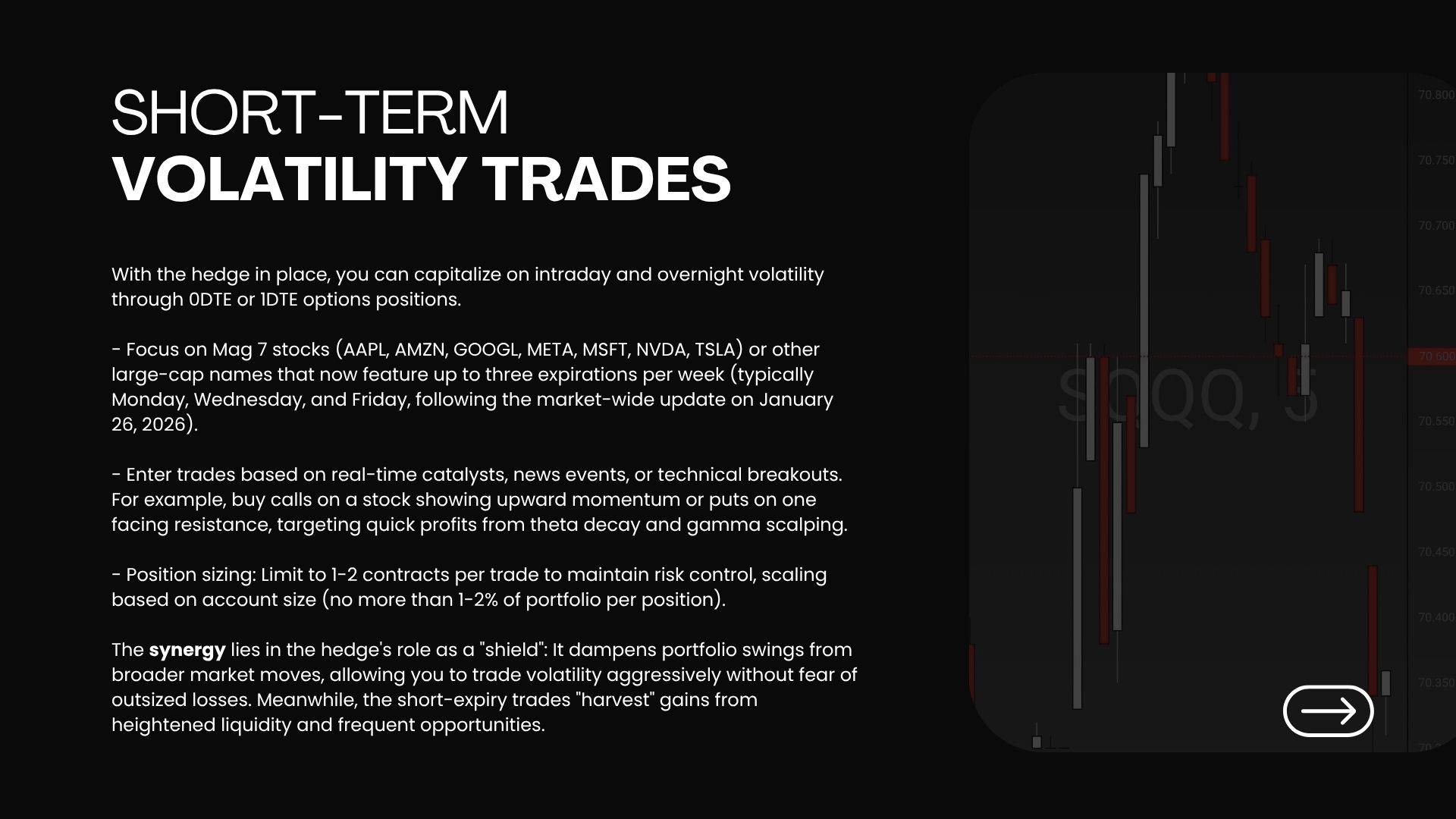

With the hedge in place, you actively trade high-frequency, short-duration positions (primarily 0DTE or 1DTE options) on major stocks like the Magnificent 7 (AAPL, NVDA, etc.) or other large caps. These exploit intraday/overnight volatility, news catalysts, or technical setups for quick gains.

Shield your capital. Exploit the volatility. Repeat.

Important Disclosure

This is for educational purposes only and not financial advice. Options trading involves substantial risk of loss. Consult a qualified advisor. Past performance isn't indicative of future results.

Explore More